Private Credit's Insurance Flywheel Exposed

E3 - Jakub Lichwa (Twenty Four AM) reveals PE insurers' virtuous flywheel fueling $3T private credit + 3 red flags regulators missed

Global life insurers have become the quiet keystone of private credit: they manage $25–30 trillion (around 8% of global financial assets), hold roughly 20–25% of the $1.5–1.8 trillion direct lending market, and yet their exposure looks manageable in aggregate while risk is building in opacity, concentrations, and capital engineering at the margins.

The Life Insurer “Savings Machine”

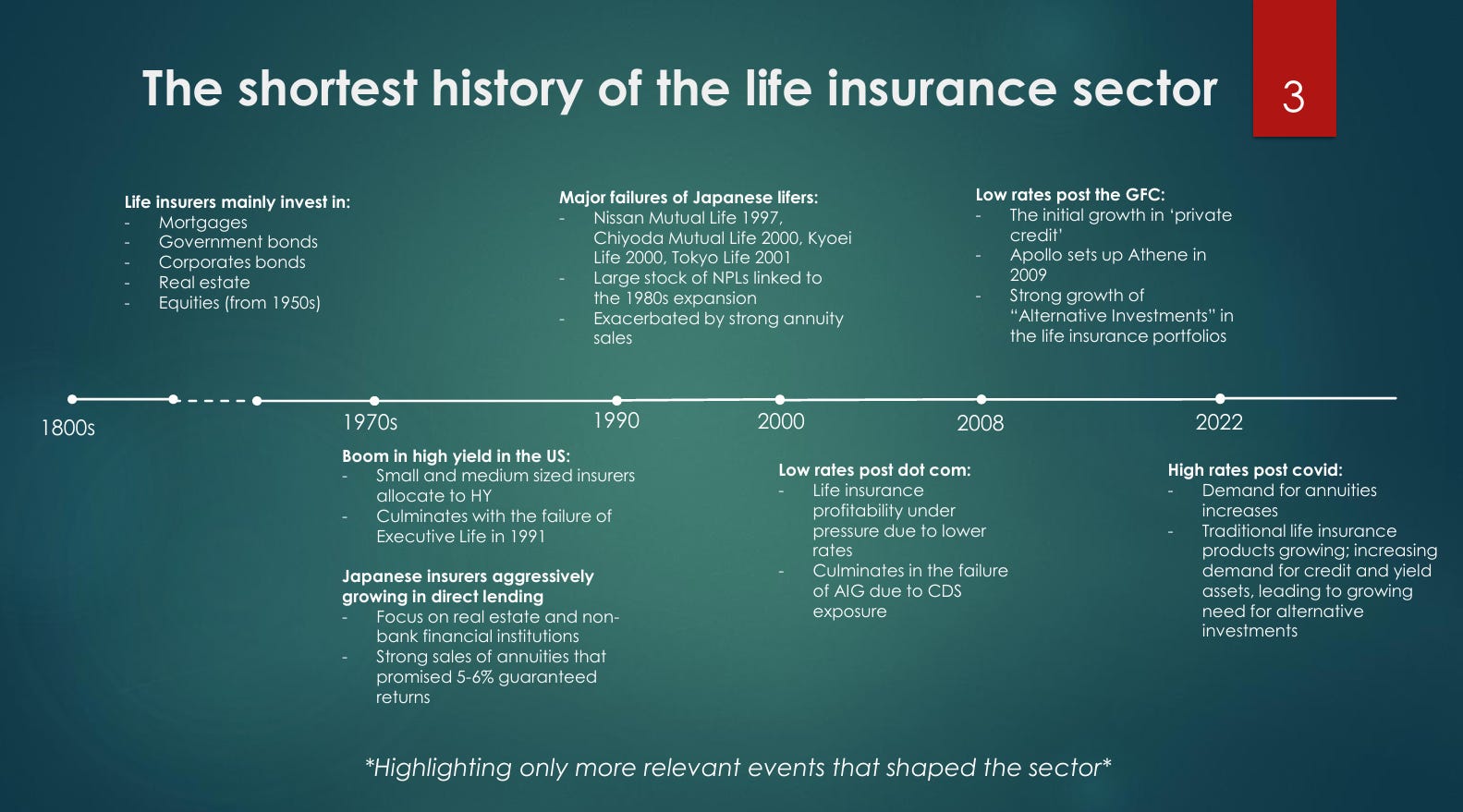

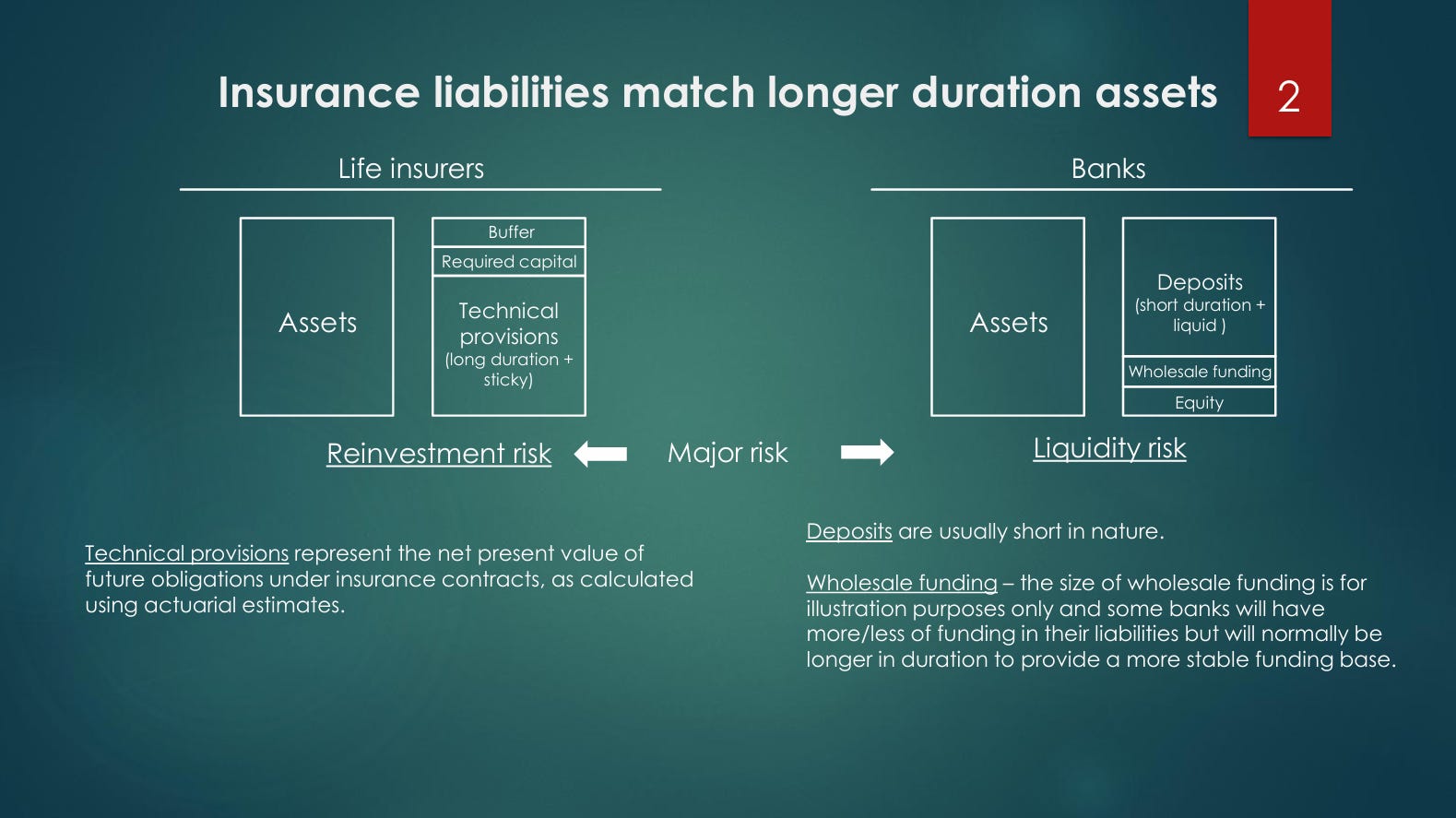

At the core of life insurance are long‑dated promises: protection products like term life earn underwriting margins on pooled mortality risk, while annuities and savings products earn a spread between portfolio yields and what is credited to policyholders. Term life shows the basic risk‑pooling logic—most policies lapse or expire before a claim is paid—while annuities can turn a lump sum at 65 into lifelong payments by pooling mortality credits, with those who die early subsidizing those who live longer. Because these annuity and savings liabilities can stretch 30–40 years or more, insurers are natural owners of long‑dated, less liquid assets, in contrast to banks that fund long loans with short deposits and primarily manage liquidity rather than reinvestment risk. History reinforces this: over 200 years, insurers have always held mortgages and real estate, added some equities post‑1950s, and periodically overreached—US junk bonds in the 1980s, Japanese real estate lending in the bubble years, AIG’s CDS book in the 2000s. The common theme is that prolonged periods of low rates force insurers to reach for yield, inflating alternatives and making them prime targets—and funding channels—for private equity.

What Private Credit Actually Is

“Private credit” is not a synonym for “alternatives,” and direct corporate lending is only half the picture. The true private credit universe spans infrastructure loans (toll roads, airports, energy), commercial real estate, capital‑relief trades and SRTs, social housing and housing associations, CLOs backed by private deals, and finally direct corporate lending in IG and HY. Alternatives is broader still, covering private equity, hedge funds, CLOs, equity-release mortgages, ground rents, real estate funds, and more. Direct corporate lending—roughly $1.5–1.8 trillion of a ~$3 trillion market—is what most headlines mean by “private credit,” and it’s also the part that has grown fastest and most aggressively. Here, outcomes depend on the borrower’s overall quality rather than project cash flows, and that matters for insurers trying to match very specific liability profiles.

Why Private Credit Belongs on Insurer Balance Sheets

Long liabilities make insurers structurally suited to hold long, illiquid credit, but the match is imperfect and full of risk. On the asset side, they hunt for bonds and loans whose cash flows mimic annuity promises, but can rarely find perfect duration matches, leaving them exposed to reinvestment risk when assets roll off. Compared to banks that manage liquidity and run risk of deposit flight, insurers deal in lapse risk instead—policyholders cancelling early—but even that is relatively forecastable over large cohorts. Against this backdrop, private credit is attractive because it can be custom‑structured: amortization profiles, covenants, and spreads can be engineered to fit liability cash flows in ways public markets often can’t. The low‑rate decade forced insurers hard into this space; after COVID, higher nominal rates reignited annuity demand and with it the need for more assets, pushing them further into mortgages, commercial real estate, and private credit just as spreads tightened.

The Global Map: Japan, US, Europe

Jakub’s key message is that you cannot talk about “the” life insurance sector; asset mixes are path‑dependent and heavily shaped by regulation and past crises.

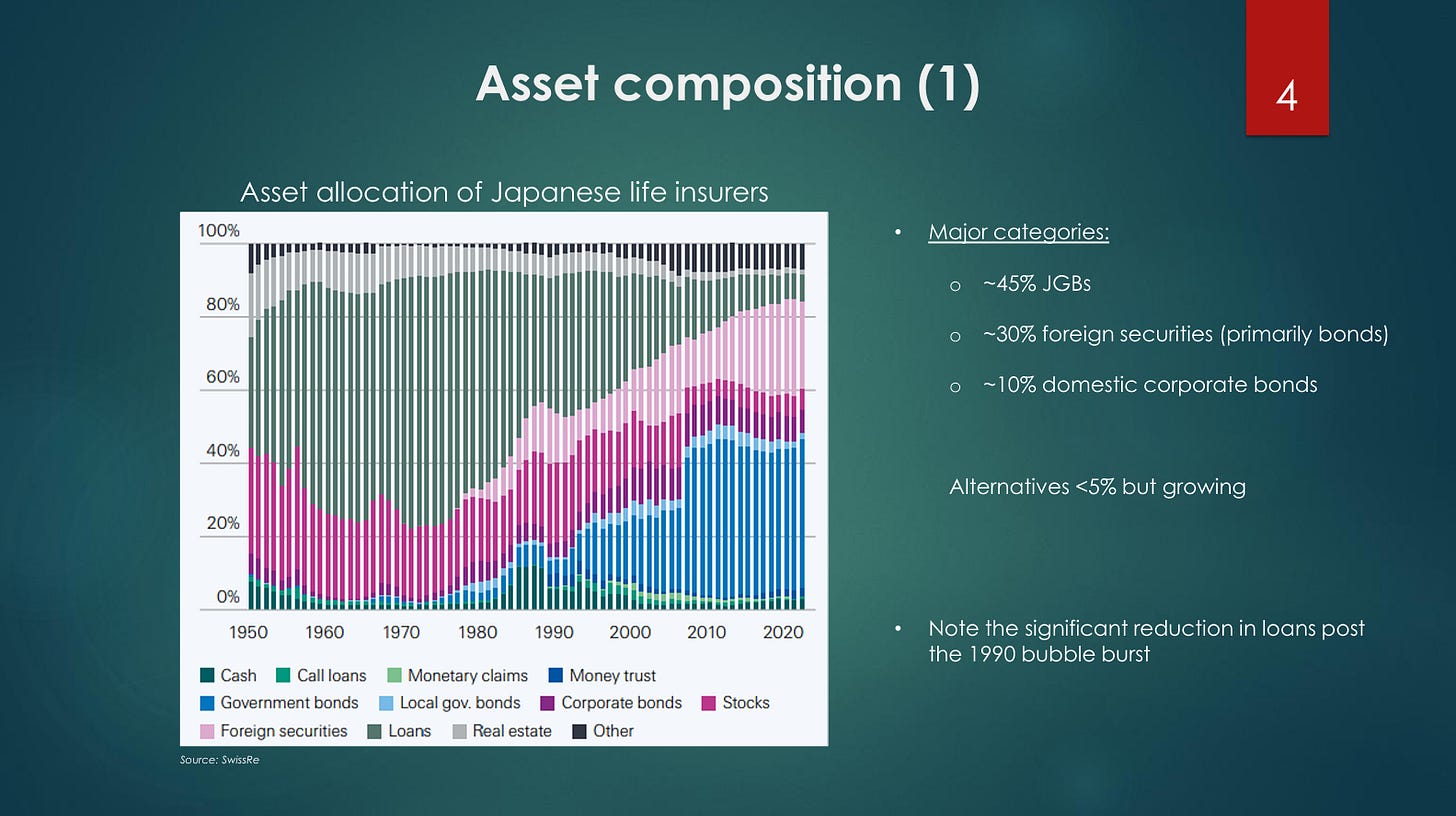

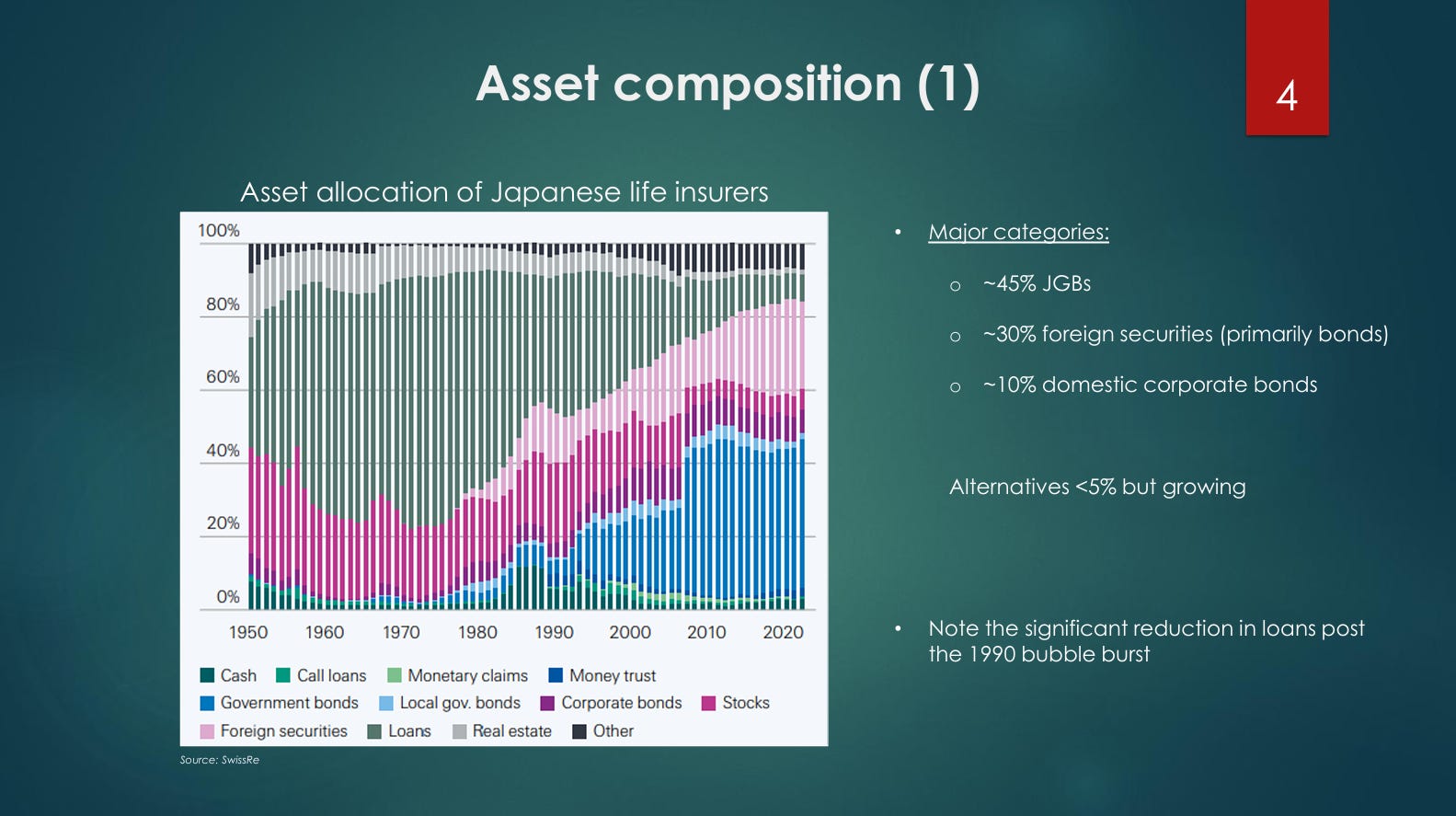

Japan: After the 1990s collapse of names like Nissan Mutual, Chiyoda, Kyoei and Tokyo Life, Japanese insurers deleveraged sharply, cut back direct lending, and rotated into JGBs and foreign bonds. Alternatives remain low (single digits of portfolios) but are creeping up, constrained by deep institutional risk aversion.

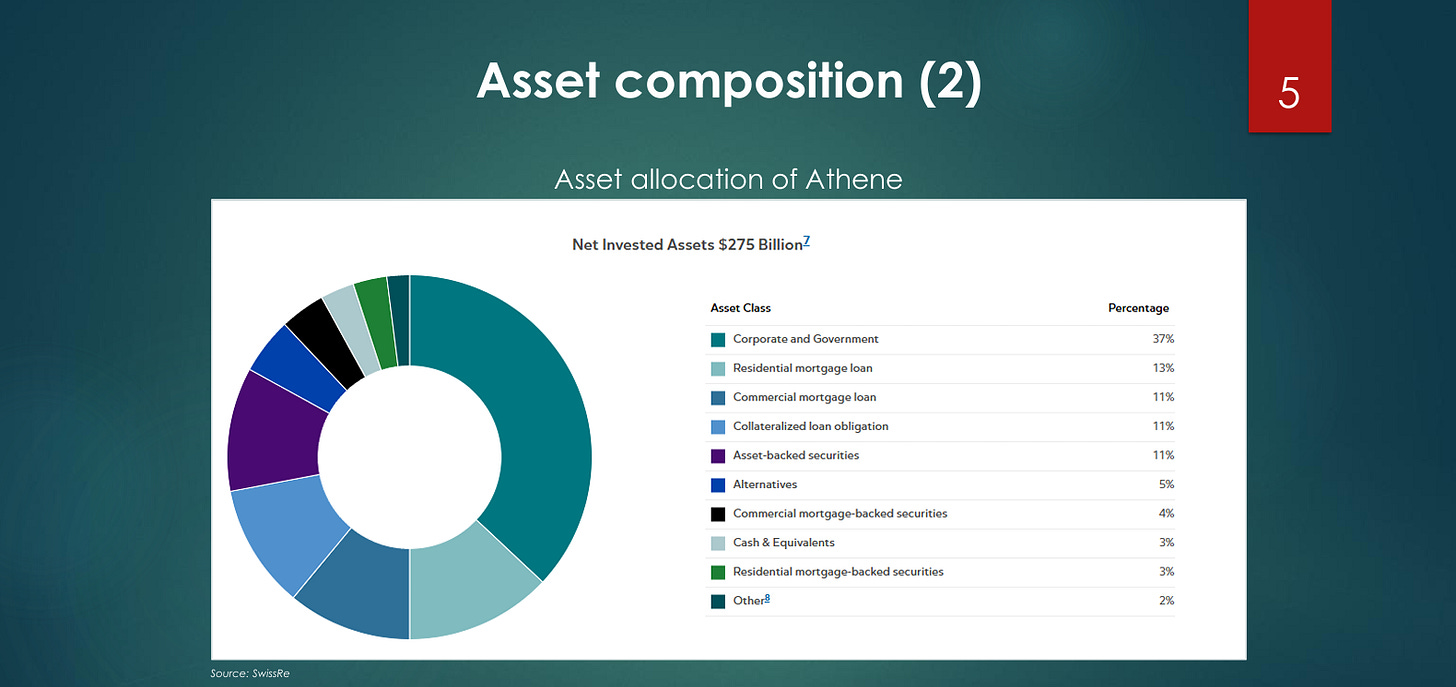

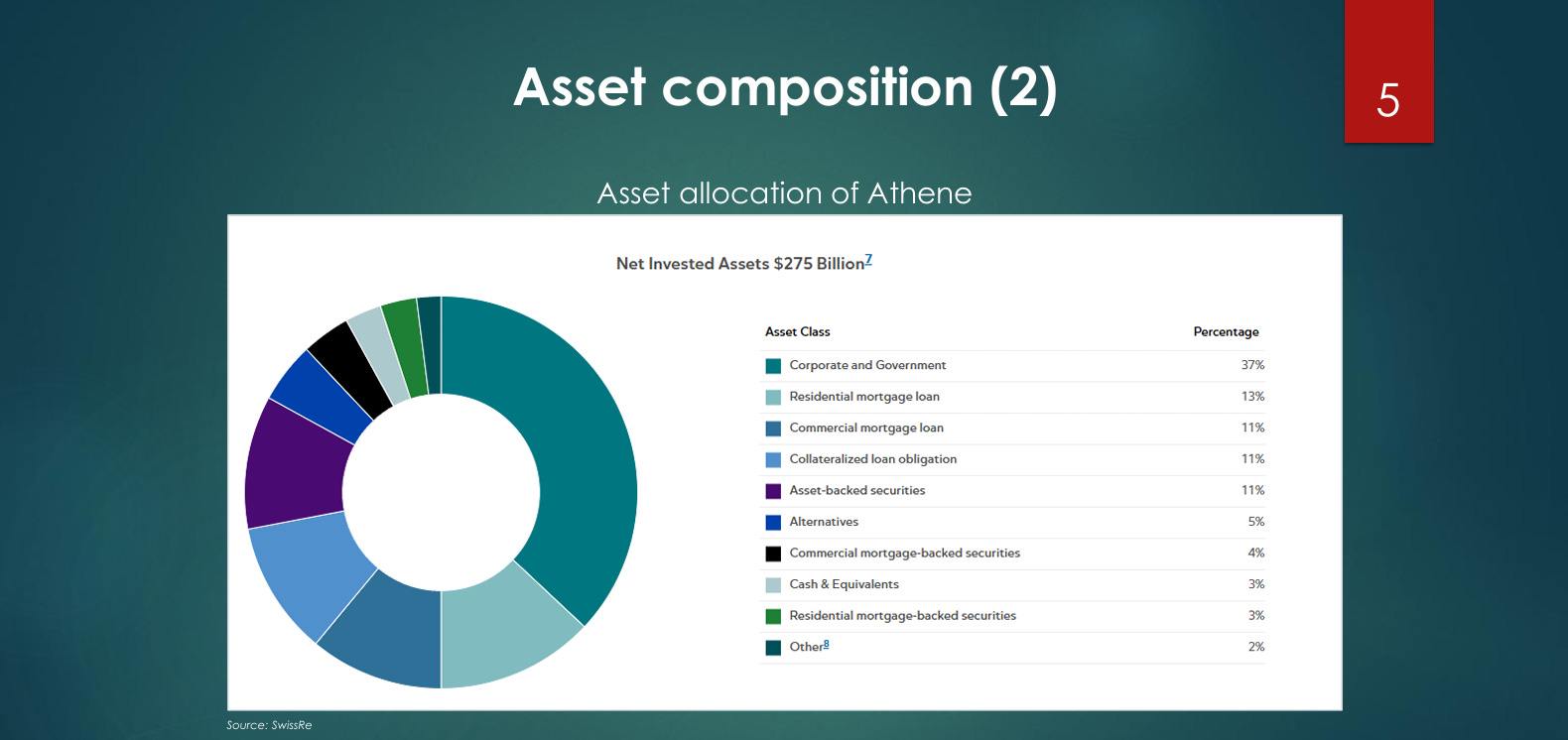

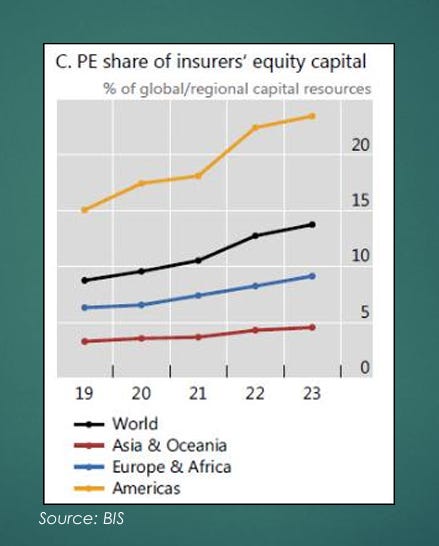

United States: US life insurers overall now carry 30–40% of portfolios in alternatives, with private‑equity‑owned platforms like Athene (Apollo) at the extreme. Athene’s statutory breakdown shows only ~37% in corporate and government bonds versus double‑digit shares in CLOs, ABS, and mortgage‑backed securities, implying much higher underlying exposure to private corporate credit than headline “less than 5% direct lending” would suggest. The US is also where PE ownership of life insurers is deepest, at around 25% of sector equity capital.

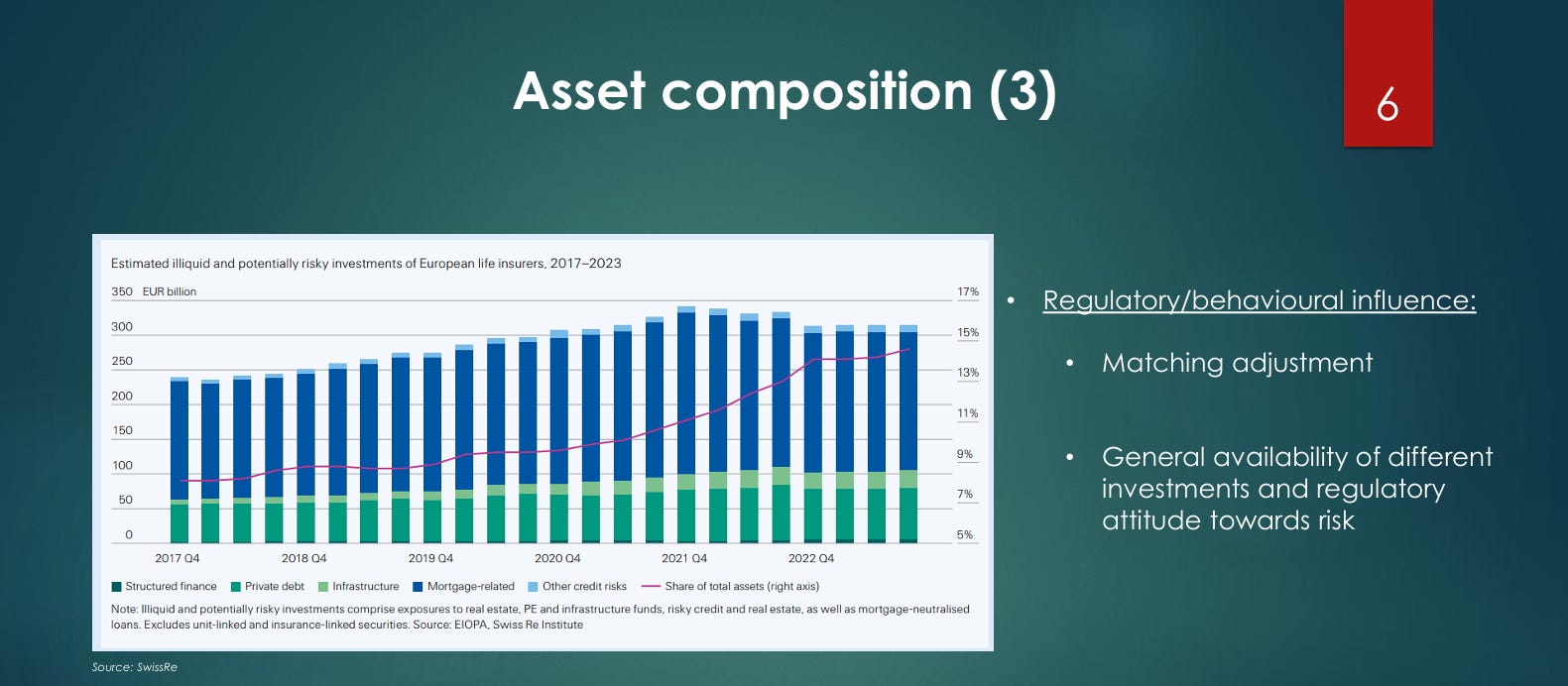

Europe: European life insurers hold roughly 15–20% in illiquid and potentially risky assets, but skewed strongly toward mortgage‑related exposures rather than corporate private credit. Regulation fragments behavior: in the UK, the “matching adjustment” regime explicitly rewards predictable cash‑flow assets that can be matched to annuities, encouraging infrastructure, social housing, and other customized private loans; in the Netherlands and France, a more mixed approach favors mortgages and some equities. The evolution of private credit has been slower than in the US, and Jakub is broadly comfortable with European insurers’ private credit exposure—at least for now.

Three Structural Red Flags: Opacity, Concentration, Growth

Jakub isolates three systemic issues around insurers’ direct corporate lending: opacity, concentration, and growth.

Opacity and disclosure gaps

By design, private credit is opaque: deals aren’t traded, documentation and borrower data are sparse, and pricing is model‑driven. Banks mitigate this with granular staging data—Stage 1, 2, 3 classifications and migrations that allow investors to track the drift of asset quality quarter to quarter. Life insurers, by contrast, present point‑in‑time snapshots of portfolio ratings with almost no visibility into how exposures have migrated between buckets, and very few disclose rating transitions at all. This sets up exactly the scenario seen in press headlines: marks that move from par to near‑zero in one step, because there was no public trail of deterioration. Psychologically, Jakub notes, this is especially toxic: humans are wired for predictability and causal stories, and opaque risk forces us to rely on trust in ratings and structures we didn’t build ourselves.Concentrations in specific players and sectors

Though life insurers’ global direct corporate lending exposure is only on the order of $300–500 billion (and perhaps ~$750 billion including broader private credit), this looks far more worrying when you zoom in on sub‑segments. Private‑equity‑owned US lifers have much higher shares of private credit—and within private credit, lending is heavily concentrated in sectors like software, embedding tech‑cycle beta into supposedly “stable” insurance portfolios. That makes losses more correlated and raises the chance that an apparently contained problem turns contagious.Breakneck growth and unseasoned books

Since 2018, US real GDP is up roughly 22%, commercial bank lending up a little over 30%, and direct corporate lending has doubled in size. On simple rules of thumb Jakub used at Moody’s, credit growth more than twice GDP as a financial‑stability warning sign; the IMF similarly flags growth only modestly above GDP as sustainable. This doesn’t mean private credit will “all turn out bad,” but it does mean that large portions of the book have never seen a recession, so loss distributions are extrapolated, not observed. In an asset class already opaque and concentrated, that is a nontrivial risk.

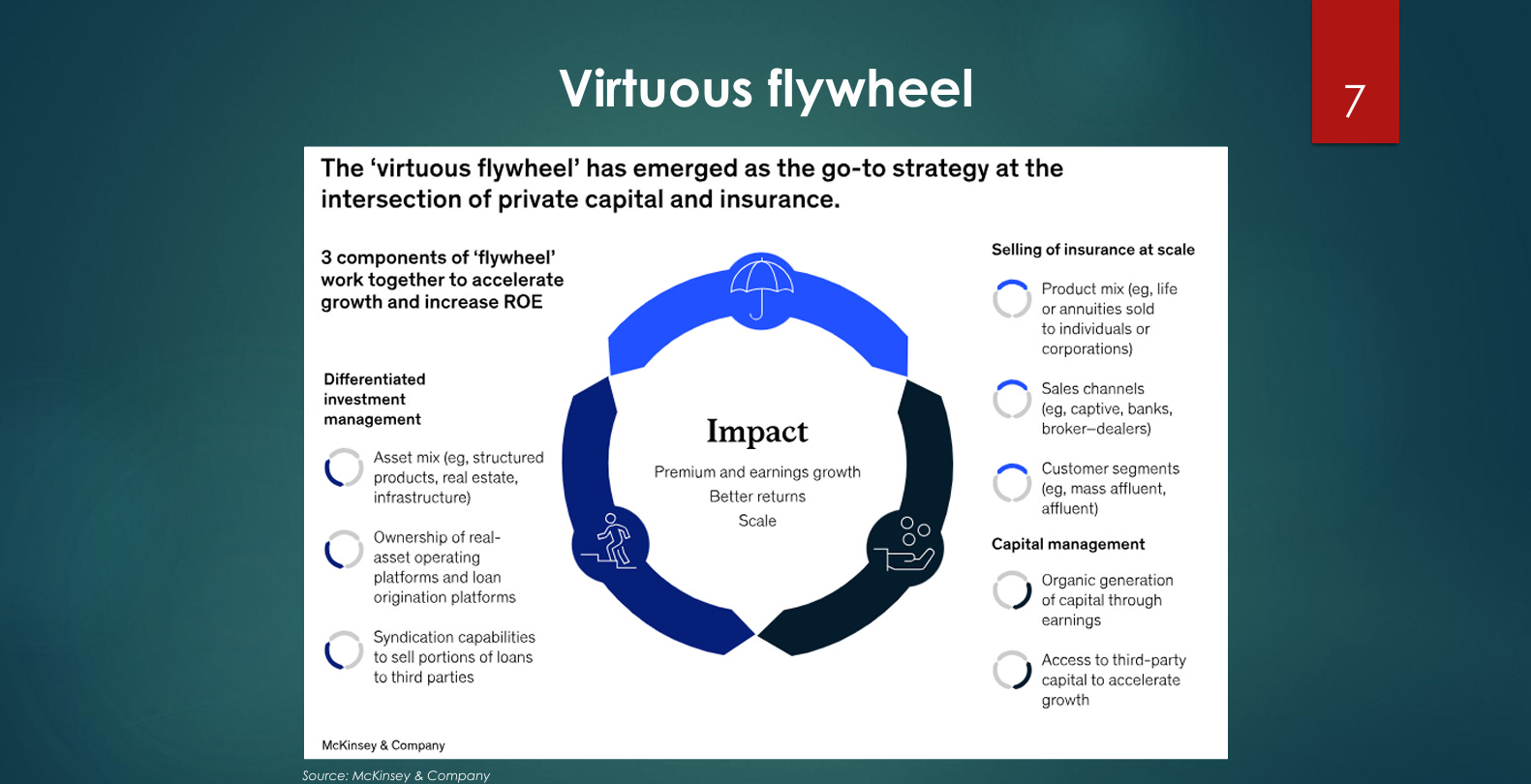

The PE–Insurance “Virtuous Flywheel”

To understand why PE firms are so determined to own life insurers, Jakub points to the “virtuous flywheel” now standard in private capital.

Selling insurance at scale

The engine is large‑scale origination of annuities and other long‑term products, either directly or by buying closed books from incumbents looking to free capital or exit lines. Each policy sold creates a long‑dated liability and an inflow of premiums that must be invested, turning the life insurer into a captive allocator of credit and yield.Capital management and sourcing

High annuity growth is capital‑intensive, so the group must secure capital via retained earnings, reinsurance, and third‑party sources like sovereign wealth funds. Over the past decade, this has evolved into increasingly complex capital‑optimization strategies, often involving offshore reinsurers where discount rates and capital rules are more favorable.Differentiated investment strategy and origination

The flywheel only works if the group can originate enough attractive assets to absorb the liability‑driven demand. That has driven the build‑out of in‑house asset managers, loan origination platforms, and real‑asset operating companies that can source, structure, and—where needed—syndicate or securitise loans. Fees from asset management and origination are incremental profit streams that reinforce the model: more annuities mean more AUM, more asset origination, and more fee income.

The strategic logic is clear: life insurers buy around 25% of private credit globally, so controlling annuity flows is equivalent to owning a privileged demand channel for one’s own origination platform. PE buyers of UK and US insurers may well see valuation upside, but Jakub believes the real prize is the moat—locking in a long‑duration buyer base for private assets structured to fit regulatory constraints.

Where It Can Go Wrong: Incentives, Cyclicality, and Reinsurance

Jakub highlights three specific red flags in the PE–insurance model: misaligned incentives, dependence on annuity growth, and aggressive reinsurance/capital engineering.

1. Misaligned incentives: Executive Life as a cautionary tale

In the late 1980s, Executive Life built close ties to Drexel Burnham Lambert, the bank that pioneered US high yield. Management loaded its general account with junk bonds—up to nearly 70% of total investments—chasing spread without adequate regard for tail risk. When the cycle turned, Executive Life failed in 1991, and the broader industry cut high‑yield exposure dramatically. There was no formal ownership link between insurer and originator; managerial affinity was enough to tilt the portfolio. The lesson is not that in‑house origination is always bad—smaller insurers often need it to access decent assets—but that close economic alignment between originator and balance sheet can skew incentives toward volume and spread at the expense of safety.

2. Reliance on annuity growth and procyclicality

The flywheel model is exquisitely tuned to a world of rising or high rates and robust demand for annuities. In that regime, strong sales grow balance sheets, fund more originations, and boost fee income for the asset management arms. The downside is a regime shift: in a recession or renewed low‑rate environment, annuity sales can drop sharply, balance sheets can shrink, and demand for new assets—and fees—falls at precisely the moment defaults and impairments are rising on the existing book. That means the business model is highly procyclical: “all is well when all is well,” as Jakub puts it, but stresses in macro, rates, and credit tend to coincide rather than offset each other.

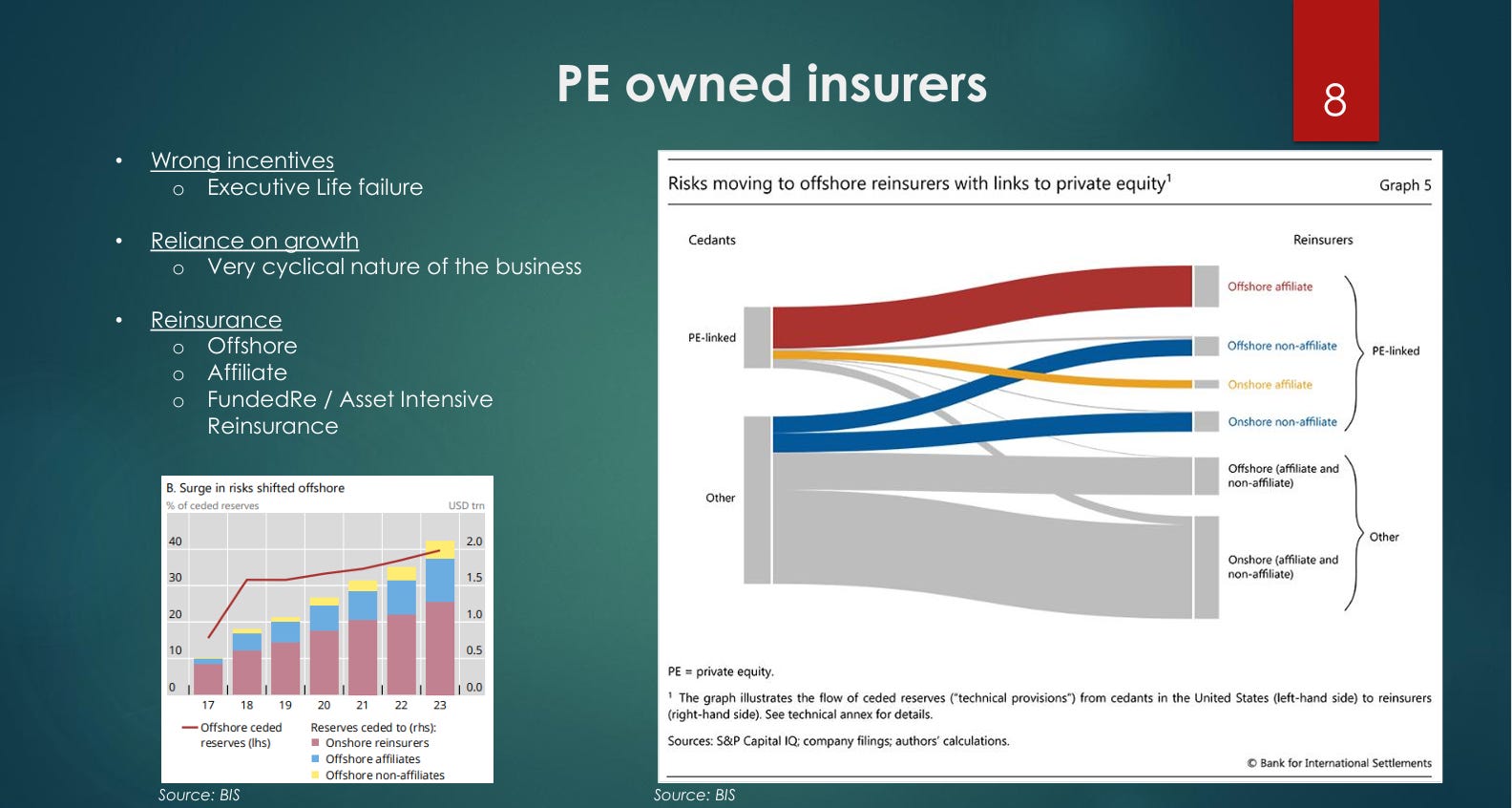

3. Capital optimisation, funded reinsurance, and offshore affiliates

Modern reinsurance tools can be benign risk transfers—or vehicles for regulatory arbitrage and opacity.

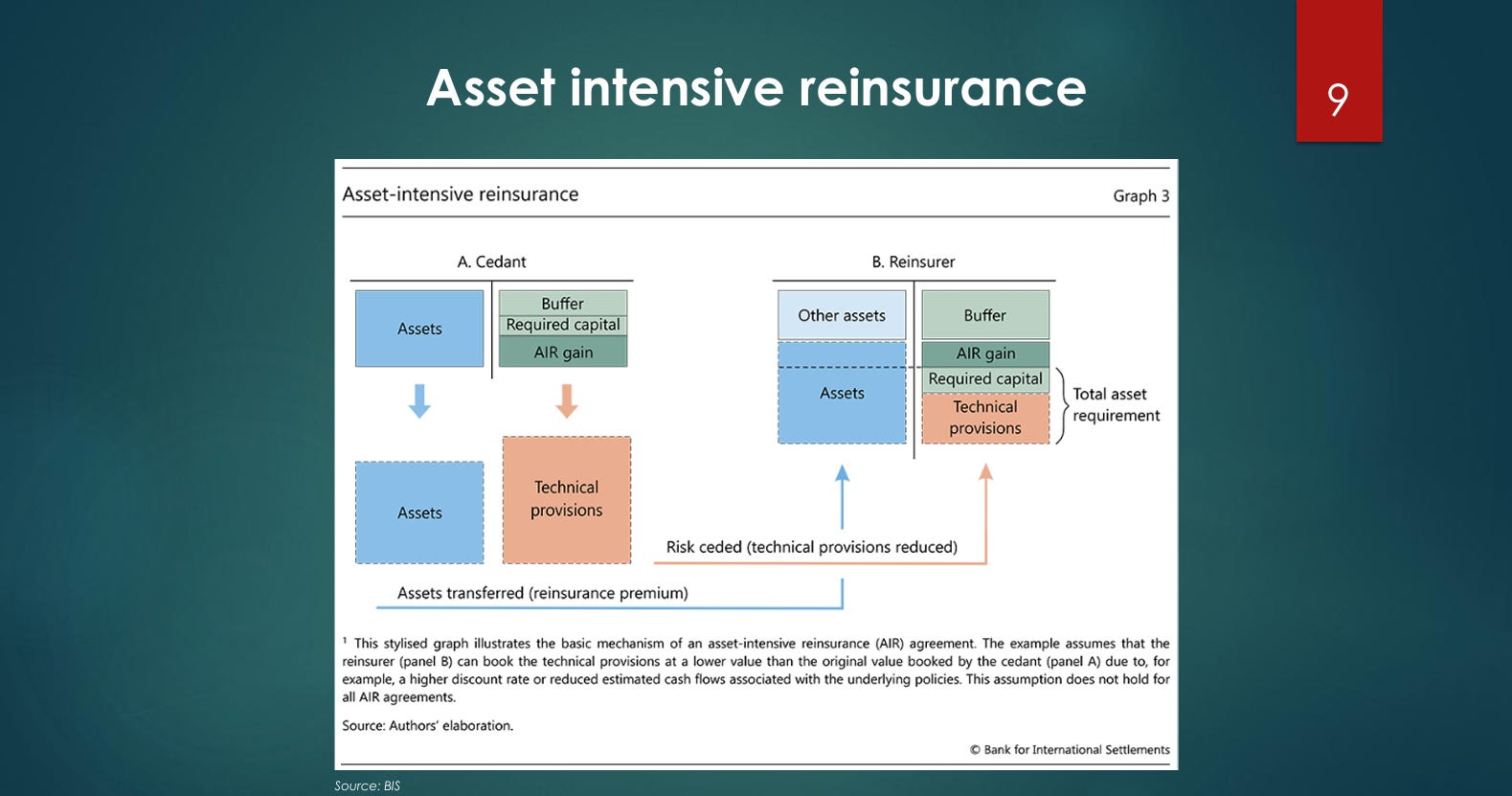

Funded / asset‑intensive reinsurance

In a traditional deal, an insurer cedes liability risk (e.g., longevity) to a reinsurer and pays a fee. In funded reinsurance, it also transfers a portfolio of assets to the reinsurer, which then reinvests into higher‑yielding alternatives such as private credit, often from an offshore jurisdiction where technical provisions can be booked at lower values. Both sides benefit on paper: the cedant frees up capital, the reinsurer harvests spread. The risk emerges if the reinsurer fails: the ceding insurer may be forced to recapture both liabilities and downtrodden assets in one capital‑intensive step. The UK regulator has already stress‑tested this risk and, for now, found only modest sector‑level capital hits—but usage is more aggressive in the US and particularly among PE‑owned insurers.Offshore affiliated reinsurers

Here, a primary insurer—say Athene—cedes liabilities to a group reinsurer in Bermuda, which invests premiums via the affiliated asset manager (Apollo), with a heavy allocation to private credit. Because the offshore entity benefits from lower capital charges, the group can hold less regulatory capital against the same economic risks than if assets were onshore. This is highly efficient from a return‑on‑equity perspective, but if pushed too far it becomes a way to game capital rules rather than to manage genuine risk, and it undermines transparency about where losses would land in stress.

BIS estimates that major US life insurers have ceded over $2 trillion of reserves (around a quarter of their total assets), with roughly 40% of this to offshore jurisdictions, and the largest users are PE‑linked groups. That doesn’t automatically imply disaster, but it does mean that a nontrivial share of risk now resides in lightly regulated or differently regulated pockets of the system.

Regional Contagion and the European Question

For now, Jakub draws a fairly sharp distinction between the US and Europe. In the Americas, private equity already accounts for roughly a quarter of insurers’ equity capital, and the integrated PE–origination–insurance–reinsurance flywheel is entrenched. In Europe, PE’s share is closer to 10%, with recent deals—Brookfield/Just Group and Apollo/Pension Insurance Corporation—marking the leading edge of that trend rather than its maturity. European asset mixes remain more conservative, especially outside the UK and Germany where mortgage‑related assets and some equities dominate the illiquid bucket. However, the logic of the flywheel and the pressure of low‑rate legacies are the same; regulators will have to decide how far UK‑style matching‑adjustment regimes and capital relief tools should go, and how closely they will scrutinise reinsurance and offshore structures. Jakub’s base case is that European private credit exposures remain manageable for now, but that contagion from US practices cannot be ruled out over a full cycle.

Listen to the full episode for Jakub’s take on Insurance and Private Credit.

This article is based on Episode 3 of Fixed + Floating, featuring Jakub Lichwa of Twenty Four Asset Management. The views expressed are those of the speakers and do not constitute investment advice. For more information on Jakub’s research, please visit https://www.twentyfouram.com/people/jakub-lichwa.

Fixed + Floating is the premier podcast for institutional investors and finance professionals exploring the forces shaping global credit markets. Hosted by Portfolio Manager Josef Pschorn, the show features conversations with leading voices from investing, research, and academia. We analyze the technical mechanics of High Yield, Private Debt, and Distressed Situations—from covenant evolution and liability management to macro policy impacts on credit cycles—providing forensic depth for the global fixed-income community.

Support Material: